A company announces it runs on 100 percent renewable electricity. The claim sounds settled, almost administrative. But ask what’s happening inside that facility at two in the morning, when the solar farm tied to the company’s renewable contract isn’t producing anything, and the picture gets more complicated. The building is still running. The electricity is still coming from somewhere. Under current accounting rules, that doesn’t matter, because the math only has to balance once a year.

This is the quiet assumption sitting underneath most corporate sustainability claims: that annual totals are a reasonable stand-in for operational reality. The GHG Protocol is now proposing to close that gap, shifting Scope 2 emissions accounting from annual matching to hourly matching. On the surface, this reads as a technical update to a carbon reporting standard. Underneath, it’s a visibility problem that has been sitting unaddressed for years, and it’s about to become someone’s project.

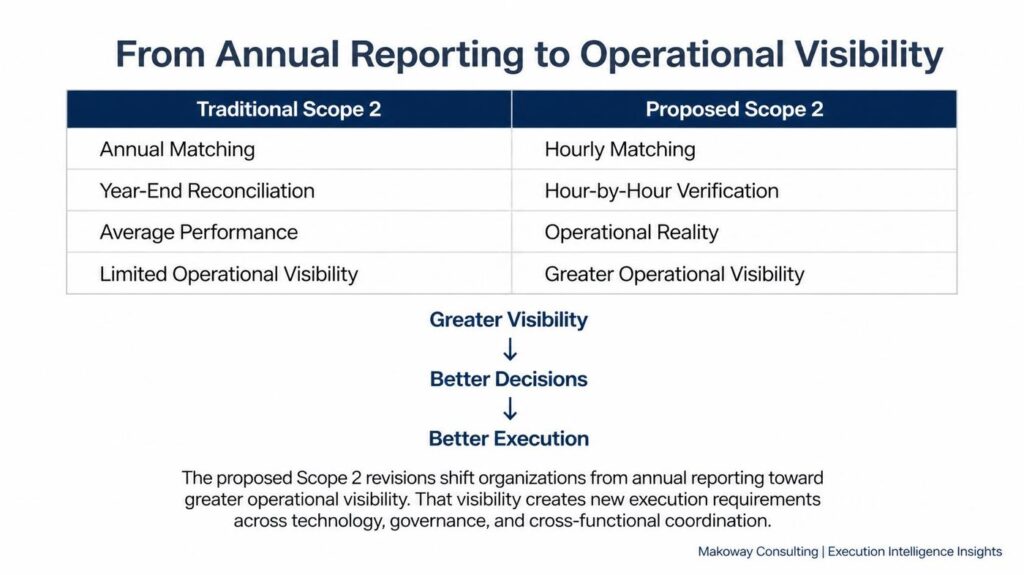

The Annual Number Was Never the Whole Picture

Organizations have been allowed to treat renewable electricity purchases as a kind of bank account, reconciled once a year. As long as the total renewable electricity purchased matches or exceeds total consumption by December 31st, the books balance. What this approach cannot show is whether the right kind of electricity was available at the moment it was actually used.

A facility running continuous operations doesn’t consume electricity the way the accounting assumes it does. Demand doesn’t pause at sundown. Supply does. The annual model absorbed that mismatch by averaging it away. Hourly matching removes the averaging and asks a sharper question: was the electricity clean when it was actually drawn, not just clean on balance across the calendar year.

This is a familiar pattern to anyone who studies execution systems. A reporting structure designed for simplicity quietly accumulates blind spots, and those blind spots stay invisible right up until someone builds a more precise way of measuring the same thing.

Why This Lands on Project Leaders, Not Just Sustainability Teams

It would be easy to file this under environmental compliance and move on. That would be a mistake.

Standards do not implement themselves. When a reporting framework changes, the organizations affected by it don’t experience the change as a policy update. They experience it as new metering requirements, new dashboards, revised data governance, supplier renegotiation, and coordination across sustainability, finance, operations, procurement, legal, and IT, often simultaneously and often without a clear owner.

None of that work happens by accident. It happens through projects, and those projects need leadership that understands both the technical requirement and the organizational friction it will create. A sustainability team can set the goal. They cannot, on their own, rebuild the metering infrastructure, retrain the reporting workflow, or coordinate five departments that have never had to share data this granularly before. That requires execution architecture, not intention.

Strategy is intent until execution begins. An organization can adopt the most ambitious hourly matching target in its industry and still fail to deliver it, not because the goal was wrong, but because no one built the system to carry it.

The Pattern Extends Past Carbon Accounting

What’s happening in Scope 2 reporting is not isolated to sustainability. The same pressure is showing up in cybersecurity disclosure, AI governance, supply chain transparency, and financial reporting. Across all of these domains, the demand is the same: stop accepting aggregated assurances and start producing granular evidence.

Regulators, investors, and customers are no longer satisfied with an organization saying it meets a standard. They want to see the system that produces the proof. That shift changes what’s required of the people responsible for delivering against these standards. Technical project management competence is no longer sufficient on its own. What’s required is enough business fluency to understand why a requirement is tightening, not just enough process discipline to execute against it once it’s been defined.

The Question Worth Asking Internally

Most organizations are watching their sustainability metrics without examining the system that produces them. That’s a comfortable place to operate from, right up until a standard changes and exposes how much of the prior reporting depended on averages rather than precision.

Before hourly matching becomes mandatory, it’s worth asking three things. Does the organization have sustainability commitments that assume a level of data granularity it doesn’t currently have. Are the projects currently underway built to support that level of precision, or were they built for the looser annual standard. And if the requirement tightens on a shorter timeline than expected, does the organization know what it would need to stand up, or would it be discovering that in real time.

The organizations that handle this transition well won’t be the ones with the most ambitious sustainability commitments. They’ll be the ones who already understood the execution system standing between the commitment and the evidence.

Makoway Consulting works with organizations to diagnose the execution systems underneath strategic commitments before they become visible failures. If you want a clearer read on where your own execution architecture has gaps, the Execution Intelligence Assessment is a place to start.